News & media Middle East Conflict and Food Inflation Through the Fertilizer Channel: Financial Risk Management Considerations

By Thiago Dalmédico Gil

Ongoing military conflict in the Middle East has the potential to generate shocks that propagate through the global food chain. In addition to raising risk aversion and disrupting logistics and trade flows, such conflict can affect agricultural markets through the fertilizer channel. Fertilizer markets are highly exposed to maritime transport, energy prices, and insurance costs, all of which are vulnerable to geopolitical instability in the region.

A disrupted critical interconnected network

Maritime shipping carries roughly 80% of world trade and operates through a densely interconnected network that depends on a small number of critical chokepoints. Among the most important is the Strait of Hormuz, which has been heavily affected by the war involving Iran. Hormuz is especially relevant for both fertilizer and petroleum markets. According to UNCTAD, the strait accounts for roughly one third of global seaborne fertilizer trade, or about 16 million tonnes, and approximately 38% of global trade in mineral fuels. Under normal conditions, around 129 vessels cross the strait each day. With the intensification of conflict, that traffic has reportedly fallen sharply to 3 or 4 per day.

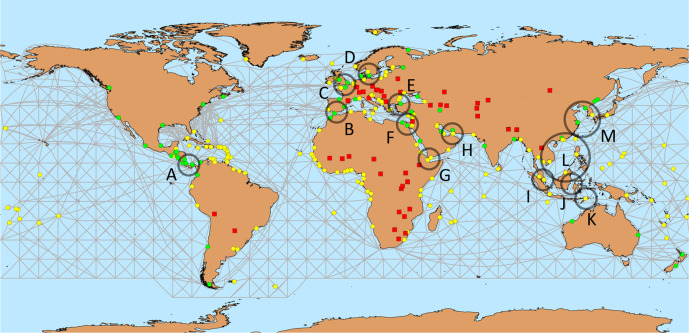

Figure 1: Global Maritime Chokepoints (Pratson, 2003)

The global chokepoint system includes: (A) Panama Canal, (B) Strait of Gibraltar, (C) English Channel, (D) Danish Straits, (E) Bosporus Strait, (F) Suez Canal, (G) Bab el-Mandeb Strait, (H) Strait of Hormuz, (I) Malacca Strait, (J) Lombok-Makassar Strait, (K) Ombai Strait, (L) South China Sea, and (M) East China Sea.

As Pratson (2023) argues, the closure of a chokepoint such as Hormuz would do more than merely redirect ships toward alternative routes. It would also cut off a substantial portion of trade for countries whose only maritime access depends on that passage. In this sense, chokepoint disruptions affect not only exporters but also importers, often with severe asymmetries across countries.

The repercussions of the disruption to the fertilizer market

This vulnerability is particularly relevant in fertilizer markets. Although a disruption at Hormuz would likely affect fertilizer prices globally, the supply consequences would be especially serious for food security in importing countries with lower resilience. Of the ten largest fertilizer importers trading through Hormuz, eight are either least developed countries or developing economies, including Sudan, Tanzania, Somalia, Mozambique, Sri Lanka, Pakistan, Thailand, and Kenya.

From a price-transmission perspective, a Hormuz disruption can affect fertilizer prices through multiple channels. First, logistical bottlenecks can directly raise the cost of moving fertilizer cargoes. Second, higher oil and gas prices can increase fertilizer production costs, since energy is a key input in nitrogen-based fertilizer production. Third, freight rates and marine insurance premiums tend to rise under heightened geopolitical risk, adding further cost pressure throughout the supply chain. The combined result is that a regional military conflict can propagate well beyond energy markets and into global agriculture and food inflation.

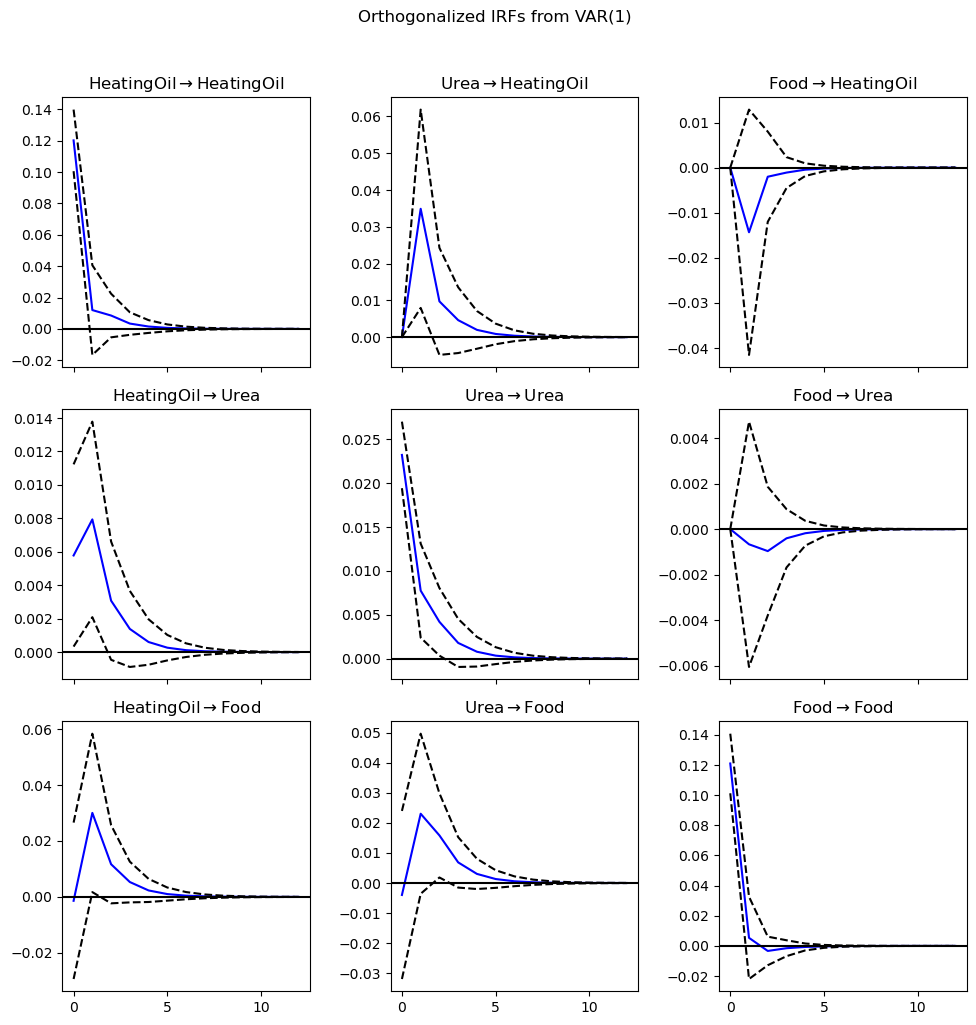

To evaluate this mechanism empirically, I model international food prices (2020-2026) using the FAO Food Price Index, fertilizer prices using urea FOB Middle East, and energy-related prices using Heating Oil futures as a proxy for refined petroleum products. The objective is to test whether changes in energy prices and fertilizer prices are transmitted to food prices over time. To do so, I estimate a Vector Autoregression (VAR) model that tracks the joint monthly dynamics of energy prices, fertilizer prices, and the FAO food index. Before estimating the model, I test whether the three series share a common long-run trend. Since the evidence does not support cointegration, the analysis focuses on short-run monthly changes rather than long-run equilibrium relationships.

The clearest result is that shocks in heating oil prices are transmitted to urea prices (urea is the most widely used nitrogen fertilizer in agriculture), and then, more weakly, to food prices. In the estimated model, an increase in heating-oil price growth in one month is associated with higher urea-price growth in the following month, and this effect is statistically meaningful. There is also evidence that increases in urea prices are followed by higher food-price inflation, although this second-stage relationship is less precisely estimated.

An impulse-response analysis reinforces this interpretation. A surprise increase in urea prices does not appear to affect food inflation immediately, but the response turns positive after one month and becomes clearest after two months. At that horizon, the estimated response of a one-standard deviation innovation on urea prices (2.3%) is about 0.016 in log-difference terms, which corresponds to roughly 1.6 percentage points of additional food-price inflation in that month relative to the no-shock baseline. The effect then fades, declining to about 0.7 percentage points by the third month.

The need for precautionary buffers for true supply-chain resilience

The food chain cannot be managed on the assumption that major disruptions are rare outliers. In practice, chokepoint risk, freight dislocation, input scarcity, and insurance shocks are recurrent features of the system, which means firms need explicit precautionary buffers rather than purely lean operating models. The supply-chain resilience literature argues that resilience is not just the ability to react after a disruption, but the adaptive capacity to prepare for, respond to, and recover from it. In other words, it’s all about the system’s ability to keep functioning under severe shocks.

In that context, holding some excess liquidity, maintaining access to backup suppliers and financing facilities should be seen not as inefficiency, but as insurance against disruptions that are uncertain in timing but foreseeable in nature.

That precaution, however, has to be matched with the right financial architecture. The corporate finance literature and practice show that firms tend to hold more cash when cash flow risk is higher, and that financing frictions make firms prefer more liquid asset structures. Firms in exposed food chains should not aim to maximize leverage and minimize idle cash at all times, but perfect debt maturity and committed liquidity so they can absorb temporary shocks without breaking commercial continuity.

Reference

Pratson, L. (2023). Assessing impacts to maritime shipping from marine chokepoint closures. Communications in Transportation Research, 3, 100083.

Bates, T. W., Kahle, K. M., & Stulz, R. M. (2009). Why do U.S. firms hold so much more cash than they used to? Journal of Finance, 64(5), 1985–2021

UN Trade and Development (UNCTAD). (2026, March 10). Strait of Hormuz disruptions: Implications for global trade and development. Geneva: United Nations Conference on Trade and Development.

Appendix

Impulse-Response Charts: Effect of one-standard deviation innovation on prices through the VAR system